“They Try to Take You for What You Don’t Have”

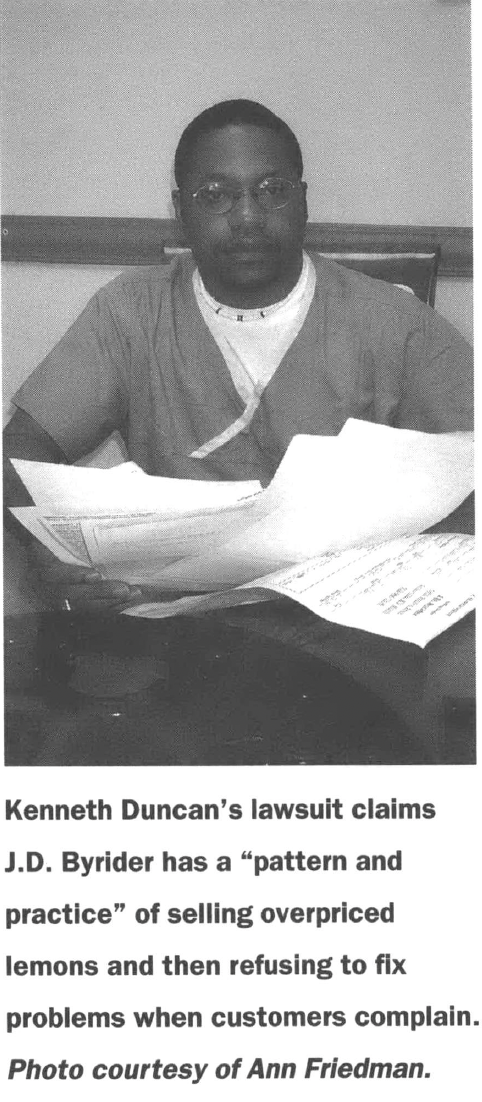

courtesy of Ann Friedman

This article originally appeared in Southern Exposure Vol. 31 No. 3/4, "Making a Killing." Find more from that issue here.

The phone rang. Another call from J.D. Byrider Sales, the used-car dealership in Louisville where Kenneth Duncan had gone to buy himself some cheap, dependable transportation.

Duncan, a low-paid nursing assistant and hospital secretary, says the woman told him: “If you don’t pay, we’ll come and get your car.”

“Come and get it?” Duncan said. “You’ve already got it.”

Duncan was already vehicle-less, he explains in a lawsuit, because the dealership had taken his trade-in, signed him to loan of almost $10,000, and then put him in not one but two clunkers: first a ’93 Grand Am, which wouldn’t start because its engine was shot, then a ’92 Oldsmobile Achieva, a replacement car that drooled a “brown, sticky substance” from under its motor and stalled so often the dealer sent a tow truck to haul it away at 11:30 at night.

According to his lawsuit, Duncan spent about three months in limbo, fending off the dealership’s collectors and fruitlessly calling to see when he could get his car back.

Finally, the suit says, the Achieva was returned to him, but the car was still a mess—it wouldn’t start, bolts were missing, oil and antifreeze were leaking, its onboard computer was lying on the passenger-side floor.

Once again, the dealership had the car hauled away. Duncan decided to fight back. He’s pushing a lawsuit that accuses J.D. Byrider of a “pattern and practice” of selling overpriced lemons and then refusing to fix them when customers invoke their service contracts.

“People like me, we don’t have a lot to begin with—if we did, we wouldn’t have to go to those car lots,” he says. “They try to take you for what you don’t have.”

Duncan’s adversary in his legal battle is no mom-and-pop gravel sales lot. It claims 90 employees, sells 300 cars a month, and is a member of the burgeoning J.D. Byrider network, which bills itself as North America’s largest used-car franchise. The national chain says it has grown to some 130 locations and sold more than 300,000 vehicles by serving the fastest-growing segment of the used-car industry—“people with less-than-perfect credit who need good cars to get on with their lives.”

Not so long ago, corporate America dismissed the used-car industry as a gritty hodgepodge of small-time operators tucked away amid pawnshops and liquor stores. But over the past decade, the industry has begun to win a place in the financial mainstream—and commenced, slowly but inevitably, to embrace the American economy’s “Bigger is Better” imperative of centralized ownership and chain-driven conformity.

Market consolidation hasn’t necessarily translated into changes in the way people get treated when they go to buy a used car. J.D. Byrider, for example, has been the target of class-action lawsuits in Ohio and Kentucky, a citizens group protest in Arizona (see “Fighting back”) and, in Louisville, a flurry of complaints to the Kentucky attorney general’s office.

Arbitration Road Block

Ann Brown of Sandusky, Ohio, sued J.D. Byrider, claiming that a wheel and axle fell off her car as her teen-age daughter was driving down the road. She claimed her contract— which included 25-percent interest and a $895 warranty fee—violated federal truth-in-lending rules and other laws forbidding fraud and unfair sales practices.

Brown never got her day in court. A judge ruled she was bound by a clause in her contract that required she seek private arbitration instead. Joan Claybrook, president of the advocacy group Public Citizen, says Brown was deprived of a shot at justice because the costs of arbitration exceeded the value of her claim. Claybrook charges J.D. Byrider and other car dealers use arbitration to insulate themselves from the legal consequences of illicit practices. Industry officials argue that arbitration is an efficient and fair way for handling complaints.

But in comments submitted to the Federal Trade Commission, Claybrook noted that J.D. Byrider retained the right to sue Brown even if she couldn’t sue the company, and said that Brown’s attorneys “have received inquiries from over 40 consumers” with complaints about the company. “Unfortunately, no matter how many of J.D. Byrider’s former customers are defrauded, they cannot file a class action because the mandatory arbitration clauses in their contracts waive their right to maintain class actions.”

One class action alleged that a cluster of J.D. Byrider franchises in Kentucky, Ohio, and Indiana hid exorbitant interest rates by charging higher base prices for automobiles sold on credit than for ones sold for cash. The lawsuit, which involved nearly 5,000 customers, was eventually settled for a modest sum, $180,000. J.D. Byrider denied any improper practices.

Kenneth Duncan’s attorney, Ellen Friedman, says she’s handled a handful of cases against the Louisville Byrider franchise, but she’s turned away many more. “Over the last three years, it’s in the hundreds,” she says. “The number of calls that I get from people with complaints is overwhelming.”

J.D. Byrider’s corporate spokesman did not return repeated calls from Southern Exposure seeking comment. In public statements, the company says it sells quality vehicles and that it treats its customers with respect. Its salespeople, it says, are “skilled at satisfying the needs of our customers.”

The costs are high—as much as 25 percent interest to finance a J.D. Byrider car or truck—but the company says that’s the price that people must pay in order to make a new start.

When a new J.D. Byrider announced its opening in Kanawha City, W.Va., this spring, franchise co-owner Bill Minsker told the Charleston Gazette: “Will people pay more? Probably. Will people have higher interest rates? Probably. But at least they’ll get something to drive.”

Minsker said J.D. Byrider helps customers clean up their credit and “get back on track establishing their freedom.”

Marc Maguire, spokesman for the Louisville J.D. Byrider franchise, declined to comment on Duncan’s lawsuit. But he says he’s willing to listen to customers’ complaints “and do what’s right.”

Maguire notes that 40 percent of his customers are return buyers or referrals from other buyers—evidence, he says, that “believe it or not, we’ve got a lot of happy customers.”

Not everyone’s happy, though. Complaints on file with the Kentucky attorney general’s office allege that the Louisville franchise and Byrider’s captive finance company, CarNow Acceptance Corp. (CNAC), engage in a variety of unseemly practices, such as selling overpriced cars that quickly break down, slipping in hidden charges, and harassing late payers with abusive collection calls.

One Louisville customer, Pamela Rankins, sent the attorney general’s office a copy of a letter she wrote to CNAC, pleading for an end to collection calls that she said were threatening and, in one instance, profane. “I’m well aware of my debt to you,” she said, “but I also have rights.”

Arm Yourself with Information

How to avoid scams and overcharges when you buy a car.

CAR PRICES

Check the CONSUMER REPORTS website, at www.consumerreports.org. Or go to a bookstore or library and look at Consumer Reports Car Buying Guide.

Ask your bank, credit union, or library to show you the KELLY BLUE BOOK, or go to www.kbb.com.

COMPARISON SHOP by checking prices in newspaper classified ads.

FINANCING

KNOW YOUR CREDIT SCORE GOING IN. Ask about your credit score at your bank or credit union, or go online at www.e-loan.com.

LINE UP FINANCING BEFORE YOU BUY A CAR. Ask an online lender, bank or credit union to prequalify you for a loan. You can usually get a better deal from a credit union or bank than a dealership. Or go online at www.e-loan.com.

If you must finance through the dealer, ASK FOR A COPY OF THE “TRUTH-IN-LENDING” STATEMENT. By federal law, dealerships and financiers are required to give you a copy, even before you sign. If they won’t give you a copy to take home and study, that’s a sign they’re hiding something.

SHOP AROUND at banks and tell them you’re comparing where you can get the best deal. When one lender quotes a rate, call others and see if they can beat it.

ADD-ONS

Dealers want to sell you all kinds of extras: credit insurance, undercoating, security systems, etc. These are almost always overpriced—and often virtually worthless. If you really need these items, you can usually get them much cheaper elsewhere.

PROTECT YOURSELF

DON’T JUST NEGOTIATE THE MONTHLY PAYMENTS. If salespeople or loan officers can get you locked into a monthly payment, it allows them to steer you into a deal with high interest and lots of add-ons. Negotiate everything: Interest rate, extras, total amount financed, etc.

READ EVERY DOCUMENT THOROUGHLY. Don’t sign anything until you’ve had a chance to think about things overnight or longer.

DON’T BE RUSHED INTO ANYTHING. If a dealership is trying to rush you, that’s a sign the deal’s a rip-off. Even if you have weak credit or little money, you have a right to be treated honestly and fairly.

PROTECT YOURSELF, STAND UP FOR YOUR RIGHTS, AND BE PREPARED TO WALK OUT THE DOOR IF A DEAL DOESN’T SMELL RIGHT.

For more information about car rip-offs, go to:

carconsumers.com

carbuyingtips.com ripoffreport.com

Another complaint came in from a 19-year-old ex-employee, Wesley Hopper, who bought a 1995 Ford Thunderbird while he was still working at the Louisville dealership. He told the attorney general that Byrider gouged him by hiking the price of his car well above its true value, and selling him a $1,095 repair warranty that he claimed was “slipped onto the papers without my authorization.”

The total cost of the deal: $8,295.

It didn’t take long, he said, before he realized the car was worth much less. “I have had the car appraised twice,” Hopper wrote. “It is worth no more than $1,200, if it is in good condition.”

But its condition was anything but good, he said. It wouldn’t start for two weeks, and he had it hauled to a garage for repairs—none of which was covered by the $ 1,000-plus warranty. When he told Byrider the transmission was about to go, he said, he was told he’d have to pay a $200 deductible before it could be fixed.

All he wanted, Hopper wrote, was to return the car and get back what he’d put into the deal—including his $700 down payment.

“Every phone call or conversation I have had with anyone at either J.D. Byrider or their finance company (CNAC),” Hopper wrote, “is filled with rudeness, sarcasm, and a direct unwillingess to help in any way.”

In response, CNAC wrote the attorney general’s office that it “would like to apologize for any inconvenience that we have caused,” but added that the case was now a “legal matter” and Hopper should contact its attorney.

CNAC’s attorney, Joe Chanda, didn’t return a phone call from Southern Exposure. After an initial telephone interview with the magazine, franchise spokesman Maguire passed word through an employee that he didn’t want to discuss the topic further.

Fighting Back

This spring in Mesa, Ariz., a small knot of protesters stood on a sidewalk outside the local J.D. Byrider store, handing out fliers to passersby and chanting “Lemon lot!” and “Deathtrap vehicles sold here!”

Dealership representatives met briefly with two customers and an organizer from the Association of Communities Organized for Reform Now. But general sales manager Rob Bartolini told the East Valley Tribune, “I believe their organization is irresponsible for just coming here and making a lot of noise when they don’t have the facts or the stories of both sides.”

It was a rare public confrontation. The well-oiled corruption of the car industry has prompted a steady flow of complaints and lawsuits, but little attention from media, politicians, or activists. The media take a timid approach to covering car dealers and financiers, partly out of fear the dealers will punish them with advertising boycotts. And state and federal legislators and many regulators have been similarly squeamish about taking on this well-moneyed industry.

“A long time ago they had agencies that looked out for the consumers,” says Delores McGee, an Upper Marlboro, Md., consumer who says she’s had legal run-ins with two of the nation’s leading “subprime” auto financiers, AmeriCredit and Credit Acceptance Corp. “Those agencies don’t exist anymore. The ones that do, you have to go through so many twists and turns just to get to them—and you wait it out, hoping they can help.”

Two years ago, U.S. Rep. Harold Ford, a Tennessee Democrat, requested hearings on discriminatory auto-financing practices, but the Republican-controlled House of Representatives has yet to take Ford up on his call.

“There’s no way representatives who get so much money from the automobile dealers and the financial industry are going to shed light on these practices,” says Rosemary Shahan, president of Consumers for Auto Safety and Reliability. “This is a source of campaign contributions for them—it comes from consumers, many of whom are getting ripped off. It means all these struggling families are donating megabucks to the Republican Party though the car dealers and the financial institutions—against their will.”

In California, consumers won a modest but hopeful victory in July with the signing into a law of a measure aimed at reining in finance-charge markups on auto loans. The new law doesn’t forbid markups, but requires dealers to keep records that allow regulators to track patterns of rate discrimination.

For consumer advocates, the wish list for reform includes laws cracking down on price gouging and fraud, more aggressive law enforcement at both the state and federal level, and a surge in activism similar to the grass-roots efforts that transformed predatory mortgage lending from a dirty secret into a national issue.

“I think what’s needed is more leadership on this,” Shahan says. “Civil rights groups should be up in arms. . . . We need to get organized. What if we say: ‘We’re really sick and tired of how you’re ripping off people. One day, when you have your huge sales, we’re not coming.’? The only language they understand is withholding money.”

Tags

Taylor Loyal

Taylor Loyal is a staff writer at the Bowling Green (Ky.) Daily News. (2003)